Market ready: How MaRS is supporting corporate moves into carbon removal

A Japanese consortium got front-row seats to the inner workings of carbon removal credit purchasing. The program helped demystify the process and build momentum in the emerging market.

We’ve got a huge carbon problem. Global emissions are still headed in the wrong direction: In 2024, levels hit a new high, and there’s little indication that the world has reached the peak of fossil fuel consumption. To keep temperatures within a liveable range, we need to see a massive ramp up of not just reduction and mitigation solutions, but also large-scale atmospheric carbon dioxide removal (CDR) technologies.

The suite of technologies that can extract carbon dioxide from the atmosphere and durably store it for hundreds of years includes such highly engineered approaches as direct air capture (DAC), the production of biochar and marine alkalinity enhancement. As many of those solutions are still being refined, the purchase of carbon removal credits by corporate buyer groups, government or other organizations is critical to the development of this sector. These purchases provide vital funding for these young CDR companies to test and scale their technologies while also helping the purchaser reach sustainability goals.

To date, the vast majority of carbon removal purchases have been made by tech and e-commerce giants, such as Microsoft, Meta, Shopify, Google and J.P. Morgan. (Indeed, these large corporations accounted for close to 80 percent of carbon removal purchases last year.) For newcomers to the space, however, “the purchasing process — at least right now — can seem overly complex and daunting,” says Niyat Gebreab, a senior associate on the climate team at MaRS. “That’s where education and collaboration can make such a difference.”

To that end, MaRS conducted a six-month-long collaboration with M-Lab, a consortium of Japanese companies, that aimed to educate members about strategies and tools so that they could begin to make their own carbon credit purchases. The program allowed the consortium to observe MaRS purchase credits in real-time, creating a safe learning space that would minimize the risks, typically associated with early market participation.

Here, with key insights taken from that program, is a primer on everything you need to know about this emerging sector and its potential impact.

What’s the difference between carbon capture and carbon removal?

While carbon capture, also known as point-source capture, traps emissions from power plants or industrial facilities, carbon removal extracts CO2 that’s already in the atmosphere. Currently, nature-based projects dominate carbon removal credits, accounting for close to 99 percent of all credit purchases. But as recent wildfires have shown, forest-based carbon sinks are exceptionally vulnerable to climate change. High-quality carbon removal solutions, such as DAC, rock weathering or water-based projects offer durable storage. They’re also measurable and often provide social and environmental co-benefits.

How much does it cost?

The price of high-quality carbon removal typically ranges between $500 to $1,000 per tonne, but as companies scale up their technologies costs are decreasing. For instance, Nova Scotia–based Planetary Technologies recently signed a $43.3-million deal with Frontier to remove more than 115,000 tonnes of atmospheric carbon over the next five years — costing approximating $371 per tonne.

Planetary Technology uses basic chemistry to reduce acid levels in the ocean and encourage the uptake of more atmospheric carbon.

What is the expected demand for carbon removal solutions in the coming years?

The potential market is massive. By 2050, it’s estimated that we will need to remove an estimated 10 gigatonnes of carbon dioxide annually.

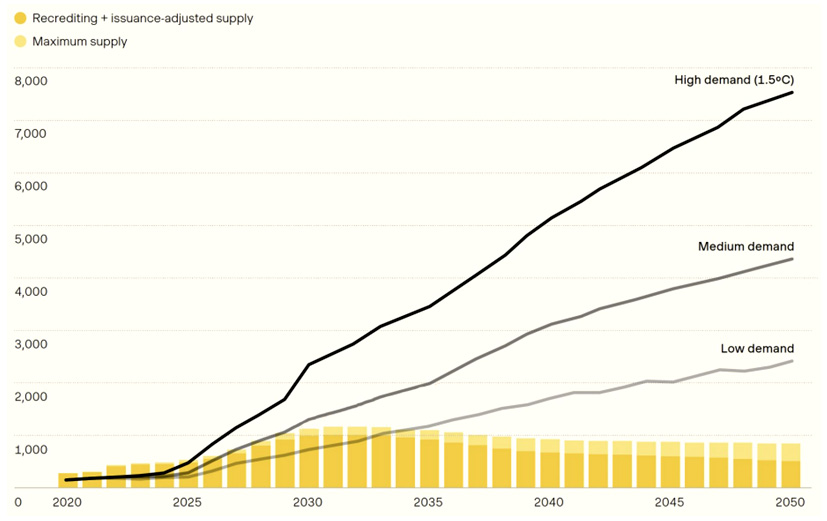

As net-zero target dates begin to approach for companies, demand for CDR credits is expected to increase exponentially, according to a recent report by Patch, a digital platform that supports the scale of high-integrity carbon markets. Demand for carbon credits could outstrip supply as soon as 2030, noted the report authors, cautioning that “companies that procrastinate until 2029 or later will find there won’t be credits to buy.”

CDRs are at the precipice of supply crisis

As Net Zero target dates begin to approach for companies, demand for CDRs will increase exponentially.

Projected supply + demand – all credits (MtCO 2e/year)

What are the biggest barriers to entering the carbon removal market?

Similar to other nascent sectors, CDR is grappling with foundational challenges that hinder broader participation. The sector is building awareness, establishing certification standards and protocols while also scaling the various technologies. Purchasers want to be confident they will get what they pay for. That can be difficult to guarantee, however, when some carbon removal technologies are still being refined. “The market is about buying outcomes — and often purchasing something that does not exist yet,” notes Gebreab. “This can be a difficult concept to grasp.”

What makes it even more challenging is that most purchasers lack deep expertise in carbon removal. While guiding M-Lab members through the purchasing process, Gebreab says it helped to discuss ways of identifying risk and how entities like certifiers and verifiers can mitigate that risk. The MaRS team also talked through how to best engage third-party verification platforms and registries, such as Isometric and puro.earth, to ensure the carbon has been removed and to certify credits.

In April, MaRS pre-purchased $120,000 worth of carbon credits from six ventures, including Vancouver-based Arca, which re-processes mine tailings to accelerate carbon mineralization.

What is motivating corporations to purchase CDR credits?

Corporations are not legally required to purchase CDR credits and what’s more, most don’t face strict mandates or consequences to reduce emissions or set net-zero targets. For companies that have set emission reduction and net-zero targets, leadership motivation, investor and employee expectations, business-to-business pressure and broader corporate responsibility trends have been the driving force.

In Japan, government-backed initiatives, like the J-Credit Scheme have also played a key role in motivating corporate action. The carbon credit program certifies greenhouse gas reductions or removals achieved through activities like renewable energy adoption, energy efficiency improvements or forest management. The certified reductions are then issued or used by companies to offset their emissions or meet sustainability targets.

What can help build corporate demand?

For many corporate buyers, it can feel daunting to leap into this evolving market. But with the right educational support, CDR credit purchases can do more than reduce emissions on paper — they can unlock real momentum in the journey toward sustainable innovation.

Through its educational program, MaRS launched a national call for carbon removal companies that could provide carbon removal credits over a period of up to three years. Cutting-edge carbon removal startups from across the country working on everything from biomass to ex-situ mineralization applied. The MaRS team then developed worksheets and a step-by-step process for M-Lab members to learn and shadow how each application is evaluated. The team was also able to draw on CDR experts, including Alexander Rink from CDR.fyi and Timothée Dulac from Puro.earth, to offer guidance on standards, registrations and certification.

“Education is essential for the many companies that are new to carbon removal,” says Rink, who is the co-founder and CEO of CDR.fyi, a database for tracking CDR credits. “Many still confuse avoidance with removal or haven’t looked closely at the benefits of multi-century durable removal versus short-lived solutions. Efforts like MaRS’s work with M-Lab help connect carbon tech innovators, corporate sustainability teams and policy experts, showing prospective buyers how to navigate the market and purchase with confidence.”

For M-Lab participants, this learning opportunity represented “an early step in their corporate journey to meet net-zero goals through Canadian carbon removal technology,” says Reina Ozaki, who is a manager of strategic partnership and business development at Mitsubishi Corporation (Americas), Silicon Valley Branch. “We’ve emerged from this partnership with MaRS with the know-how to begin making our own purchases in the future.”

Does Canada have an edge in this sector?

Canada has an excellent opportunity to be a world leader in durable CDR solutions, says Rink, “particularly as we anticipate it evolving into a true commodity market — an area of historical Canadian strength.” The country is also achieving critical mass in this area: There are 40 organizations currently working on carbon removal initiatives across the country, and a quarter of the finalists for the global XPRIZE Carbon Removal challenge for CDR innovation are Canadian.

Plus, Rink adds, Canada already “boasts ample natural resources that enable key methods (for instance, biomass supply for BECCS and biochar, geological storage to sequester DAC and other methods, rock formations for enhanced weathering and coastlines for various marine approaches), an expanding pool of CDR suppliers, a strong research ecosystem and supportive federal policies. This combination of tangible resources, an innovation-friendly environment, and a credible brand puts Canada in an excellent position to welcome worldwide suppliers as they explore and scale up carbon removal solutions.”

How can business leaders best support this emerging market?

Business leaders who are interested in getting involved should tap into existing resources, rather than “re-inventing the wheel,” says Gebreab. Many leading buyer organizations, such as Frontier, have made templates and resources freely available to prospective buyers. MaRS, for example, drew on Shopify’s Buying Carbon Removal, Explained and Carbonfuture’s Guide to Carbon Dioxide Removal Policy to shape its own supplier evaluation process and criteria, while Frontier’s purchase agreement and application form templates reduced the administrative burdens for suppliers. Some suppliers had already applied for purchases from Frontier and could repurpose their applications for the MaRS procurement, saving time and effort.

Leaders can take other practical steps, such as connecting with MaRS to join future Carbon Credit Education and Purchasing Programs. They can also partner with buyer groups (Frontier, NextGen and Milkywire) or connect with advisory and marketplace organizations (Carbon Direct, Patch and Watershed) or knowledge organizations (CDR.fyi, Carbon Business Council, Pembina Institute and Carbon Removal Canada) to help fill knowledge gaps.

“These are solutions that will make a tangible impact on planetary health,” says Gebreab. “It’s so rewarding to see the sector gain momentum with more and more leaders eager to jump in.”

To find out more about carbon removal technologies, read this recent MaRS report.